SDBA: Professional Management for Your 401(k),403(b), 457 Plan

There is very little argument that it is important to start retirement savings early, and to keep doing it. However, approximately 40% of plan participants are not confident that they know what their personal investment selections should be; and about 30% experience a lot of stress in selecting their 401(k) investments.1 The 403(b) is the corresponding plan for tax-exempt organizations, as found in educational institutions, hospitals, or religious groups. The uncertainty and stress levels are common in the nursing population as well.

The financial information company BrightScope found the average number of investment options in plans in 2014 to be 22. This includes counting all of the various series of Target Funds available as a single option.2 So, there is a fair amount of information to review. In addition, one prominent study by AON Hewitt, Help in Defined Contribution Plans: 2006 through 2012, found that retirement savers who pursued some form of investment advice through their plan had a median annual return that was almost 3% higher than those who did not. These results also accounted for fees paid for this advice. This help could have been in the form of target-date funds, managed accounts, or online advice.3

One feature that many do not know about is the availability of a self-directed brokerage option, or window, that may be a part of a 401(k), 403(b), or 457 plan. It may be available in as many as 40% of plans today. In addition to the selected fund options that exist in a retirement plan, the self-directed brokerage account (SDBA), would make it possible for a participant to buy individual stocks, exchange-traded funds or other mutual funds. It typically has had very little participation, as most participants still must work through financial decisions with little expertise. However, because of the self-directed window, other programs have been developed that feature professional managed portfolios and strategies. In keeping with the fiduciary focus in the industry today, these advice driven programs may also incorporate risk criteria in the construction of these portfolios.

In an effort to provide more choice, flexibility, and professional management, numerous employers have augmented their plans with the SDBA option. Many of the prominent health and educational institutions have the window available. These include Adventist Health, Cedars-Sinai, Dignity Health, Kaiser Permanente (both Physicians & Management, and Nurses & Staff), and the University of California Retirement System. This might seem like yet another item to think about. However, so many participants do not really start “planning their plan” until after they are out of their company plan or the workforce. This concept can provide an earlier start for participants to receive real guidance with some portion of their plan.

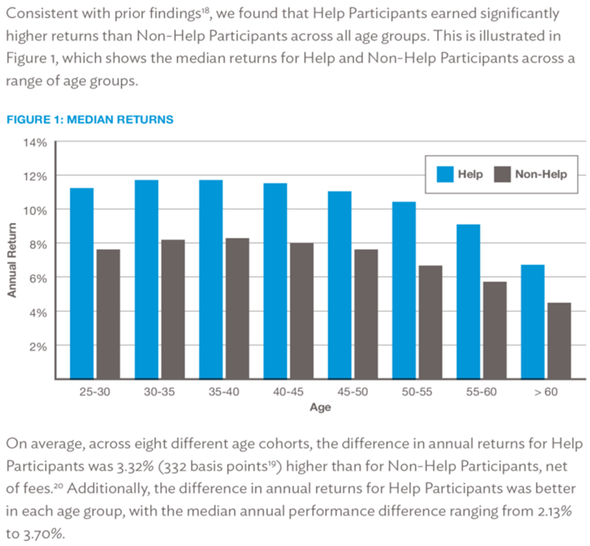

The following is a graph of the AON Hewitt study measuring median returns of retirement plan savers with and without some form of professional investment help. 4

18 The first edition of this report, Help in Defined Contribution Plans: Is It Working and for Whom?, was published in January 2010. The second edition, Help in Defined Contribution Plans: 2006 Through 2010, was published in September 2011.

19 100 basis points = 1%.

20 All returns reported in this research are net of fees, including fund-specific management and expense fees and managed account fees where applicable.

As the chart indicates, there was a significant annual return difference between those participants who received help and those who did not. The data in this study from 2006 through 2012 is consistent across all age groups; which is worth some reflection. The upside to all of this is that you don’t have to do manage your retirement plan all by yourself.

You are encouraged to review your own retirement plans, to ask us questions at any time, and to learn more about the various tools available.

1 2015 401(k) Participant Survey conducted by Koski Research for Schwab Retirement Plan Services, Inc. Respondents participated in the study between May 26 and June 3, 2015.

2 The BrightScope data is based on IRS Form 5500 filings by private sector defined contribution plans with audited financials. These are generally larger plans, those with more than 100 employees.

3 Help in Defined Contribution Plans: 2006 through 2012. The study of 14 large retirement plans with more than 723,000 individual participants and over 55 billion in assets, by Aon Hewitt, a consulting firm, and Financial Engines, an investment advisory firm, between 2006-2012. Published May 2014.

4 Help in Defined Contribution Plans: 2006 through 2012, p.14.